Across the United States and worldwide, flooding is the deadliest and most costly natural disaster. The U.S. National Flood Insurance Program (NFIP) is an imperfect framework for reducing flood losses, but currently the best we’ve got. The NFIP is scheduled for Congressional reauthorization in 2017, and this debate promises to be lively. The Natural Hazards Research and Mitigation Group at University of California, Davis has been analyzing NFIP databases, examining patterns over the history of the program and focusing on flood losses and insurance, particularly in California.

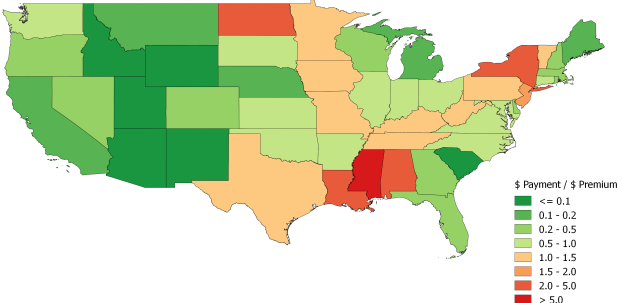

Over the history of the NFIP, the state is one of a few that have – through dry years and wet – received only a fraction of payments from the program compared with the premiums it has paid in. Since 1994, NFIP damage payouts in California have totaled just 14 percent of premiums collected (compared with 560 percent for the biggest recipient state, Mississippi). For California, this imbalance exceeds $3 billion over 21 years – funds that could have been invested in risk reduction, floodplain management and reduced premiums.

California has unparalleled expertise and a culture of progressive solutions for managing its flood risk; the state also has unique needs and intense pressures looking forward. With the NFIP facing an uncertain future – more than $20 billion in debt, and with a challenging Congressional reauthorization discussion looming in 2017 – we recommend a careful look at California’s place in the NFIP. In particular, the state should now explore its own flood insurance program, with savings invested in long-term risk reduction. Properly implemented, a state-based insurance program and proactive flood mitigation strategies could through synergy benefit the environment, agriculture, recreation and water resources. This approach has major challenges, with implications for California and nationwide that should be explored.

Background

The NFIP was established in 1968 to curtail development on U.S. floodplains and along our coasts. Previously, homes and businesses were being built on flood-prone land almost without restraint. Flood damages were multiplying out of control, and private insurers had stopped offering flood coverage to homeowners and all but the largest businesses. As disastrous floods struck through the 1950s and 1960s, victims had nowhere to turn but the federal government, and U.S. taxpayers saw spiraling payouts for disaster relief. The NFIP established a grand compromise: if communities passed ordinances to limit new construction on floodplains and coastlines (and other activities worsening flood damage), then the federal government would help provide flood insurance in those communities. Today the NFIP underwrites more than 5 million policies, providing more than $1.25 trillion in coverage, taking in more than $3.5 billion a year in premiums. The program has limited but not halted floodplain development. Yet flood losses have continued to climb, and the NFIP is now more than $20 billion in debt.

We examined nationwide databases of NFIP flood-damage claims dating back to 1972, annual policies since 1994 and records of properties with multiple payouts (what the Federal Emergency Management Agency terms “severe repetitive loss.” These data include property characteristics, insurance claims and the nature of flood losses. Some attributes were stripped from the databases to maintain policyholder anonymity. We combined NFIP data with other GIS (Geographic Information Systems) data, such as income and social vulnerability, to examine affordability and equity of NFIP coverage.

California, Flood Risk and the NFIP

Despite more than a century of investment in controlling flood threats – including $11 billion in flood management projects over the past decade – California still has massive flood-risk exposure, according to the Department of Water Resources. Statewide, roughly 7 million people are at risk from flooding with a threat to $580 billion of buildings, public infrastructure and crops. Of 81 major disaster declarations in the state since 1954, 45 involved flooding.

The Central Valley is the most flood-prone area of the state, a threat addressed during the past 100 years by the construction of levees, bypass channels and upstream dams. In recent decades, developers and local officials have engaged in a tug-of-war with floodplain managers and flood-risk researchers, with local interests promoting new development on California’s floodplains behind levees, some of them strengthened and providing high levels of protection (others less). However, no levee provides complete protection – “There are two kinds of levees … [t]hose that have failed and those that will fail” (Martindale and Osman, 2010). Levee projects accompanied by additional floodplain development often increase total risk and flood liability.

To counterbalance this threat, California has 290,000 NFIP policies in force, covering nearly $82.6 billion of insured assets, and generating $212.8 million in annual premiums (data to Oct. 31, 2016). These totals include residential, commercial and some government properties on river floodplains and along coastlines. The NFIP also insures properties outside mapped flood-hazard zones, roughly one-third of all policies nationwide. The U.C. Davis analysis of the NFIP data is ongoing, and interesting patterns are emerging in the California data and the full U.S. dataset. Two conclusions have jumped out of the analyses completed to date that seem timely and pertinent to state and federal policy discussions.

Ratios of claim payments to policy premiums in 1994–2014, by state (in 2015 dollars). (California Water Blog)

Repetitive Losses

Thirty years after the establishment of the NFIP, the Higher Ground report (National Wildlife Federation, 1998) singled out a problem – a small number of “repetitive loss” properties were receiving repeated insurance payouts, accounting for a disproportionate share of all NFIP outlays. At that time, just 2 percent of all insured properties drew 40 percent of all disaster payments. One property in Houston received 16 payouts totaling $806,591 – more than seven times the structure’s value.

Our U.C. Davis research group, working with the Natural Resources Defense Council (NRDC), also looked at repetitive flood-loss properties. New FEMA data show that 30,369 properties (0.58 percent of NFIP policies) – designated “Severe Repetitive Loss” (SRL) properties – are responsible for 10.56 percent of all claims. (Our request to FEMA for its broader “Repetitive Loss” [RL] database is currently pending.) Current SRL properties include structures that have each been the subject of up to 40 flood-damage claims. One house in Alabama, valued at $153,000, has received $2.25 million in NFIP payouts – more than double the highest ratio in 1998 (the Houston property discussed above).

The NRDC has proposed incentives to remove repetitive-loss properties from the NFIP insurance and the nation’s floodplains. Hayat and Moore (2015) propose that “property owners should agree in advance not to rebuild following floods that cause substantial damage and, instead, to accept a government buyout of their property and relocate. In exchange, they would receive a discount on their federal flood insurance coverage.” We are now working to identify communities with repeated flood damages, high densities of designated SRL properties and high socioeconomic need. Implemented carefully, such proposals could reduce the most burdensome flood-loss properties, while improving insurance affordability and transitioning low-income residents off the floodplain.

Of the more than 30,000 SRL properties nationwide, 393 are in California. At the top of the list, Louisiana has 7,223 such properties and Texas 4,889. Nonetheless, the California SRL properties amount to $56.7 million in cumulative payments. More detailed examination suggests there are local issues in California – Sonoma County ranks 20th among communities nationally for the largest number of SRL claims (977) and 25th for total SRL payments ($27 million). California leads the nation in many metrics of flood protection and resilience, but local problem areas may require additional guidance, resources and/or oversight.

NFIP Net Payers and Net Recipients

Flood insurance requires that many participants pay into the program in any given year so a few may draw funds in times of extreme need. Health, auto and home insurance, too, may include low-risk participants who persistently pay into the program pooled with higher-risk participants. These variations are sometimes addressed by setting premiums proportionate to estimated risk, but sometimes the risk factors are too difficult to quantify or are simply accepted as a subsidy to some in the insurance pool.

The NFIP is rife with subsidies, such as low “grandfathered” premiums for homes built in floodplain and coastal flood zones before the start of the program or repetitive-loss structures that resist attempts to mitigate or relocate off the floodplain. Our analyses of NFIP historical policy and claims data suggest that such imbalances and subsidies also exist at a state-to-state scale, and should be examined carefully.

The U.C. Davis analysis examined NFIP claims and premiums data between 1994 and 2014. Calculated as ratios of total premiums paid to total claims, some U.S. states emerged as long-term recipients of NFIP funds and other states as long-term payers into the program. Over these 21 years, Mississippi policyholders paid 18 cents per dollar of flood insurance payouts, whereas Wyoming policyholders paid $32 in premiums for every $1 in claims.

Implications

A major policy question is whether “net payer” states have just been lucky (having avoided major floods in the last 21 years). Or has flood risk in these areas been overestimated or successfully managed or reduced, so that these states subsidize the larger insurance pool?

Several mechanisms could explain why some U.S. states may have better managed flood risk. These are the subject of ongoing research. If verified, these states may want to look to remedies that credit their investments, attention, enforcement and/or more diligent stewardship of their floodplains and coastlines. However, the penalty for getting the above question wrong may be severe.

Preliminary analyses suggest that California consistently pays more into the NFIP than is justified by historical damage claims.

Since 1994, the program’s damage payouts in California total just 14 percent of premiums collected. The three most damaging flood years in NFIP history have all occurred since 1994, and yet only the worst year of California flooding (1995) has cumulative NFIP payouts exceeding premiums collected statewide, and then only slightly ($1.35 in claims per $1 of premiums).

Furthermore, a community-scale analysis of payout/premium patterns shows that only 18 of California’s 538 jurisdictions had cumulative NFIP payouts exceeding premiums collected in that area. And 119 jurisdictions, or 22 percent of California’s total, paid NFIP premiums over the full duration of study, but had zero payouts. One region – the Central Valley – has been particularly outspoken about perceived unfairness in costs and restrictions imposed by the NFIP (for example, Government Accountability Office, 2014). Although we do not accept all claims of “floodplain exceptionalism” suggested by some Central Valley residents and growers, initial analyses suggest high NFIP premiums relative to historical claims – payouts are just 9 percent of cumulative Central Valley premiums. More detailed analyses of agricultural structures and flood losses are needed.

Policy Recommendation

California should explore a state flood insurance program, with potential savings invested in long-term risk reduction.

Current federal law requires that home and business owners with federally backed mortgages must carry flood insurance. However, this mandatory insurance need not be through the NFIP. In the past two to three years, more private insurers have selectively offered flood coverage. There is broad interest in privatization of flood insurance, including pending federal legislation (H.R. 2901 and S. 1679), but concern exists from floodplain and flood-risk experts that privatization will reduce FEMA funding for floodplain mapping and mitigation activities. Perhaps more concerning is that private insurers will “cherry-pick” flood policies now overpriced by the NFIP and leave the program as the insurer-of-last-resort, holding only grandfathered, repetitive-loss and other “actuarial dogs” imposed by legislative mandate. This outcome would overwhelm the NFIP with unsustainable debt.

Rather than relying on privatization to solve its flood insurance inequities, California should move quickly to stake its place in this arena. This recommendation was earlier made by California’s Department of Water Resources in 2005: “Examine existing flood insurance requirements and consider the creation of a ‘California Flood Insurance Fund,’ … to compensate property owners for flood damage.”

California should consider acting before private interests make state action untenable. Interesting public-private solutions are possible, such as partnering with private reinsurers to hedge the risk from low-probability, high-magnitude catastrophic floods. Many services funded by the NFIP, such as flood-hazard modeling and mapping, are being done across California using tools half-a-century ahead of FEMA-funded contractors.

California also leads the country in implementing flood mitigation measures, such as bypass channels and levee setbacks, that simultaneously reduce flood risk for surrounding areas, enhance riparian and wetland habitats, promote agriculture, provide recreation and support groundwater recharge. In implementing its own flood insurance program, California would be in a position to address many of the shortcomings of the NFIP, remedying important issues like repetitive-loss properties, residual risk behind levees and sovereign liability for flood damages.

California is in a position to do what it does best – not follow the nation, but lead. The state has the expertise, and the need, to set new precedents in sustainable flood-risk management.

This story originally appeared on California Water Blog, a publication of the U.C. Davis Center for Watershed Sciences. You can read it here.